![90s.pm.investing [EN]](https://substackcdn.com/image/fetch/$s_!gwa6!,w_120,h_120,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F101bbd96-f32d-47f3-bb0e-9c76efa580c0_1054x1054.png)

Broadcom (AVGO) — Research Analysis

Hypothesis-Driven | Mutually Exclusive | Collectively Exhaustive

I. Who Is Broadcom (AVGO)?

Broadcom Inc. (NASDAQ: AVGO) is a mega-cap semiconductor and software conglomerate that has rapidly transformed from an “M&A-driven analog chip company” into a “full-stack AI infrastructure platform.” Its lineage traces back to 1961, when Hewlett-Packard established its semiconductor products division, HP Associates. In 2005, KKR and Silver Lake Partners acquired this semiconductor unit from Agilent Technologies for $2.66 billion, forming Avago Technologies, and brought in Malaysian-American entrepreneur Hock Tan as CEO.

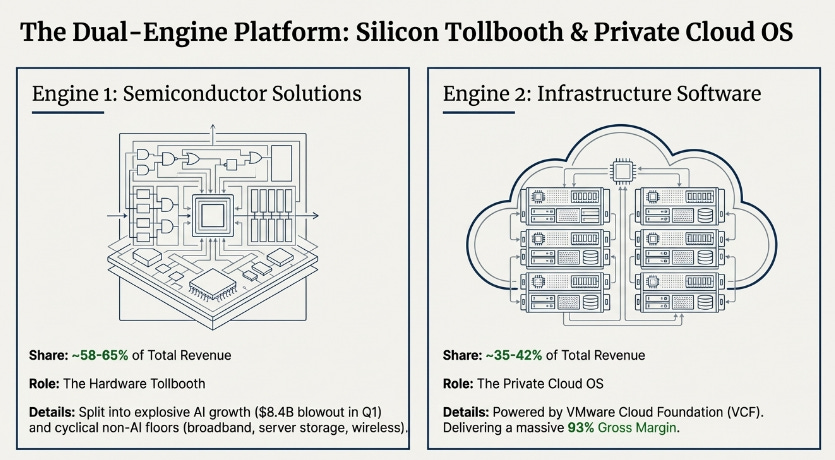

If Nvidia’s core DNA is “general-purpose GPU compute platform + CUDA developer ecosystem,” then Broadcom’s dual-engine model rests on “custom AI accelerators (XPUs) + silicon content dominance in Ethernet networking” combined with “VMware/VCF as the enterprise infrastructure software control plane.” The former is now growing at 106% year-over-year and has become the “toll booth” of AI infrastructure; the latter, with a 93% gross margin and high-stickiness subscription model, provides a stable, recurring cash flow base.

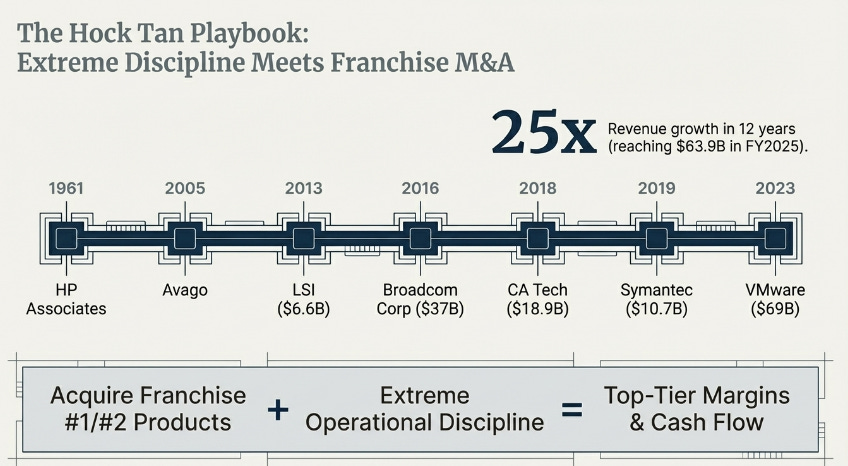

Hock Tan has been dubbed “the Warren Buffett of semiconductors” on Wall Street. His playbook is not to build products from scratch internally, but to execute a series of large-scale acquisitions, targeting companies with “franchise products” — those holding the #1 or #2 market position with high switching costs — and then applying operational discipline to drive margins and cash flows to industry-leading levels. From the 2013 acquisition of LSI ($6.6B), the 2016 acquisition of the original Broadcom Corp ($37.0B), the 2018 acquisition of CA Technologies ($18.9B), and the 2019 acquisition of Symantec’s enterprise security business ($10.7B), to the 2023 completion of one of the largest transactions in tech history — the $69.0B acquisition of VMware — Broadcom’s revenue has soared from $2.5B in FY2013 to $63.9B in FY2025, a more than 25-fold increase over twelve years.

Today, Broadcom commands a market capitalization of approximately $1.55–1.70 trillion and has been characterized by some observers as the newest member of the “Magnificent Seven” (replacing Tesla). The company is not a traditional cyclical semiconductor business, but rather a “digital infrastructure toll booth for the AI era”: on one side, designing custom AI chips and high-speed networking for the world’s largest hyperscalers (Google, Meta, OpenAI, Anthropic, ByteDance, and others); on the other, providing the private cloud and private AI software foundation for Fortune 500 enterprises globally.

We reject fairy tales — we draw our tree with science.

II. How Does Broadcom Make Money?

Broadcom’s revenue structure can be decomposed into two “stacked” cash engines, alongside an AI accelerator business that is rapidly reshaping the company’s overall profile.

Semiconductor Solutions

This is Broadcom’s primary revenue engine, contributing $36.86B in FY2025 (57.7% of total), and rising to approximately 65% of total revenue in Q1 FY2026. It is further divided into two key blocks:

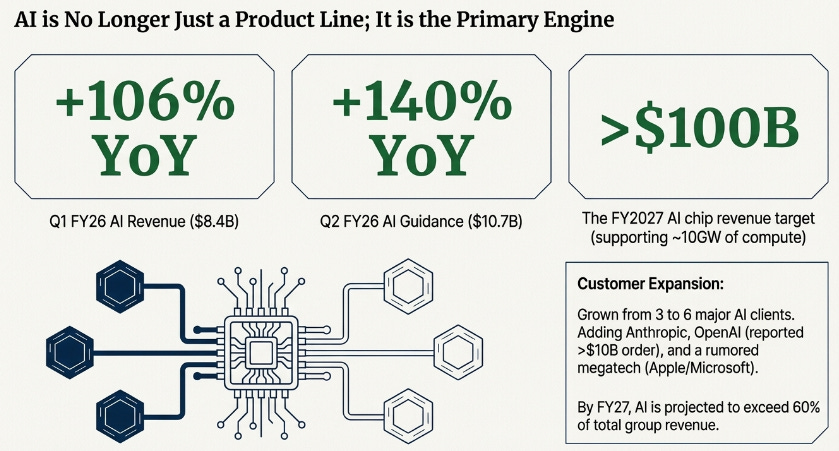

AI Semiconductors (Custom XPUs + AI Networking): Full-year FY2025 AI revenue reached $20.2B (+65% YoY), and surged to $8.4B in Q1 FY2026 (+106% YoY). Broadcom designs custom AI accelerators (XPUs) for Google (TPU), Meta (MTIA), OpenAI, Anthropic, and others, while also providing Tomahawk switch chips (the world’s only 100 Tbps-class device), 200G/400G SerDes, PCIe switches, and optical DSPs covering the full AI networking silicon stack. CEO Tan has noted that AI networking’s share of total AI revenue is rising from 33% to 40%, signaling that Broadcom is not merely an “XPU design house,” but a provider of silicon content across the entire AI rack.

Non-AI Semiconductors (Broadband, Server Storage, Wireless, etc.): Q1 FY2026 revenue of approximately $4.1B (flat YoY), currently at a cyclical trough, with modest recovery in broadband and server storage. This segment includes WiFi/Bluetooth chips for Apple and other consumer electronics clients, enterprise broadband equipment, and industrial semiconductors.

Infrastructure Software

FY2025 contributed $27.03B (42.3% of total); Q1 FY2026 came in at $6.8B. The core of this segment is VMware — acquired for $69.0B in 2023 — together with the earlier acquisitions of CA Technologies mainframe software and Symantec enterprise security.

VMware Cloud Foundation (VCF) is Broadcom’s flagship software product — the “operating system” of the enterprise data center, virtualizing CPU, GPU, storage, and networking into a unified private cloud environment. Broadcom has fully transitioned VMware from perpetual licensing to a subscription model, and in VCF 9.0 has incorporated Private AI Services (GPU monitoring, model store, Agent Builder, vector databases) as standard subscription entitlements. With a software gross margin of 93% and operating margin of 78%, this segment serves as the company’s primary cash flow stabilizer.

The AI Accelerator Is Reshaping the Entire Business

The most critical structural shift is that AI semiconductor revenue is evolving from “a product line within a division” into “the primary engine driving the entire company.” Q1 FY2026 AI revenue of $8.4B already represented 43.5% of total revenue, and Q2 guidance of $10.7B in AI revenue implies an even higher share. CEO Tan has set a FY2027 AI chip revenue target of “significantly above $100B,” corresponding to approximately 10 GW of compute deployment — implying that by FY2027, AI could contribute over 60% of group revenue.

III. What Has Broadcom Been Up To Lately?

Q1 FY2026 Blowout Results: AI Revenue Doubles, Guidance Raised Again

The Q1 FY2026 results reported on March 4, 2026 represent one of the most impressive quarters in Broadcom’s history: total revenue of $19.31B (+29% YoY), with AI semiconductor revenue of $8.4B (+106% YoY), both surpassing consensus expectations. Even more striking is the Q2 guidance: total revenue of ~$22.0B (~+47% YoY) and AI semiconductor revenue of $10.7B (~+140% YoY), indicating that AI growth is not decelerating — it is in fact accelerating. The stock surged more than 6% in after-hours trading following the announcement.

From 3 Clients to 6 Clients: Expanding AI Customer Base

Broadcom has confirmed that its AI XPU customer base has grown from 3 hyperscalers in FY2024 (Google, Meta, ByteDance) to 6 customers, adding Anthropic, OpenAI, and one undisclosed client (widely rumored to be Apple or Microsoft). The OpenAI engagement is reportedly valued at over $10B, making it one of the largest single AI contracts in Broadcom’s history.

$73B AI Backlog + Supply Chain Locked Through 2028

Broadcom’s AI-related order backlog has reached $73B (nearly half of its combined backlog of $162B), with delivery scheduled within 18 months. CEO Tan has also confirmed that Broadcom has secured advanced-process wafer capacity (TSMC), HBM memory, and advanced packaging substrate supply through 2026–2028, ensuring supply constraints will not become a bottleneck.

VMware Subscription Migration Nearing Completion; VCF 9.0 Launches the “Private AI Platform” Chapter

Over 87% of large-enterprise VMware clients have already transitioned to subscription-based VCF contracts, with CEO Tan projecting completion of the remaining conversions in approximately 18 months. VCF 9.0 officially incorporates Private AI Services as standard subscription entitlements, shifting Broadcom’s narrative from “monetizing software via price increases” to “making VCF the singular platform for enterprises to run private AI.” Nine of the top 10 Fortune 500 companies are already using VCF, with over 100 million core licenses deployed globally.

Dual-Track Deleveraging and Capital Return

Total debt has declined from ~$69.9B in August 2024 to ~$64.2B, with net debt/EBITDA at approximately 1.6x. In January 2026, Broadcom issued $4.5B in senior notes to extend near-term maturities out to 2031–2056. Fitch upgraded Broadcom’s credit rating to BBB+ with a Positive Outlook. In parallel, the company announced a new $10B share repurchase authorization (through year-end 2026) and raised the quarterly dividend 10% to $0.65/share.

🗺️ Investment Assumption Map (AVGO | Broadcom)

Level 0: What Is the Core Question This Investment Is Asking?

At a current stock price of approximately $317–338, a market capitalization of ~$1.55–1.70T, and a valuation of Forward P/E ~31x, TTM P/E ~66.7x, and PEG ~0.87, the market is essentially assuming that Broadcom is “a core beneficiary of AI infrastructure buildout” — while debating whether growth can be sustained, whether valuation has fully discounted the trajectory, and the extent to which customer concentration and COT (customer-owned tooling) risk caps the long-term upside.

The mispricing opportunity lies in whether the market is excessively pessimistic (or insufficiently constructive) in its pricing of:

The pace of AI networking share expansion and full-stack silicon content uplift (the market still perceives Broadcom primarily as an “XPU design house” rather than a “monopolistic provider of silicon across the entire AI rack”)

The qualitative transformation of VMware/VCF from a “pricing uplift windfall” to a “durable private AI platform with high stickiness” (is this a one-time migration effect, or a sustainable ARR growth engine?)

The timeline of COT (customer-owned tooling) risk (is the market discounting a 5-year-out risk into today’s share price?)

Level 1A: Is the Market Large Enough? Is the Structure Favorable? Who Controls the Toll Booth?

(Is the market treating “AI semiconductors” as a homogeneous, commoditized market — thereby overlooking Broadcom’s dual control points in custom ASICs and high-end networking?)

A1.1 [AI Demand Structure]: Is AI infrastructure spending a multi-year, multi-customer, cross-use-case (training + inference) structural platform buildout — or a single-cycle, excess-procurement event concentrated among a handful of hyperscalers?

A1.2 [Control Point vs. Substitute]: Is Broadcom’s AI value proposition derived from substitute demand during a GPU shortage (a scarcity premium) — or from customers’ structural preference for custom XPUs + full-stack IP + supply chain lock-in (a control point premium)?

A1.3 [VMware AI Demand Durability]: Can VCF evolve from a “one-time revenue re-rating driven by pricing and forced migration” into the “standardized platform for enterprise private AI,” generating sustainable ARR growth?

Level 1B: Is the Business Model Profitable? Are Cost Advantages Sustainable?

(Is the market assuming that AI semiconductor volume ramp inevitably compresses gross margins — analogous to DRAM or commodity chips — thereby overlooking the operating leverage embedded in Broadcom’s fabless + design IP model?)

B1.1 [AI Semiconductor Gross Margin Resilience]: Can AI semiconductor gross margins remain stable, or experience only modest dilution, during a rapid volume ramp — reflecting the structural distinction between a fabless + design IP model versus an integrated device manufacturer with captive fabs?

B1.2 [Software Subscription Revenue Quality]: Has VMware’s perpetual license-to-subscription transition genuinely improved ARR predictability, gross margin profile, and customer lock-in effects?

B1.3 [Capital Allocation Discipline]: Can Broadcom continue to deleverage, sustain high shareholder return rates, and maintain balance sheet health — even while scaling AI investment and integrating VMware — without sacrificing financial discipline in pursuit of growth?

Level 1C: How Durable Is the Moat?

(Is the market over-discounting the long-term possibility of customer-owned tooling (COT) into a near-term threat — one that is already partially priced into today’s valuation?)